.png)

Yes. It is a good time to buy a house in Barre, VT. How’s that for a short answer!

Here’s why it’s a good time to buy a house in Barre, VT.

There’s more inventory than we’ve seen in many years. The number of sales isn’t dropping compared to recent history, it’s just that there are more people putting their homes on the market in Barre. Not just Barre, that trend is holding for Montpelier, Waterbury, and many other towns in Central Vermont as well.

So, with the number of sales holding steady, and the number of new listings in Barre increasing, supply and demand is going to predict that there should be some good buys out there. Or at least some good properties that you don’t feel are massively overpriced.

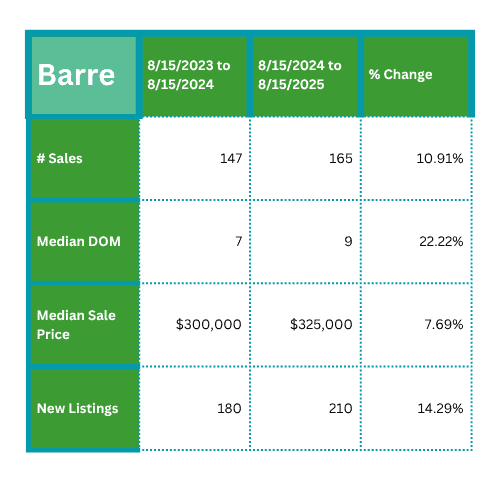

Want a side order of data?

This data is for Barre City and Barre Town. For this article, calling the market “Barre” is valid. Sales are higher this year compared to the previous 12 month period, but the number of new listings is up even more. Again…more inventory.

As of this writing, there are 30 homes in Barre that are active and on the market. That’s a lot to choose from! The prices range from $115,000 to $1.75m, and the median listing price for homes that are currently for sale in Barre is $289,500.

For reference, the national average sale price for existing home sales was around $435,000 earlier this summer.

We’re also seeing median sale prices rising at a slower rate than in recent years. I know, as a homebuyer in Barre, hearing that sale prices went up 7.69% doesn’t sound great. It sounds like homes are getting more expensive. They are. But…in 2022-2023, median sale prices in Barre went up by 11%. Which makes 7.69% seem a lot more appealing.

Just remember that once you own a home, you’re probably pulling for those higher price increases. It’s ok to change what you want.

Interest rates are pretty similar to what they were a year ago, so that’s not much of a variable. Generally, buyers are looking at 6.25%-6.5% for 30 year fixed rates.

Is it a good time to buy a house in Barre, Vermont? The numbers say yes. Of course, everyone’s situation is different. There are lots of good reasons to buy a home–including being in control of your housing stability, asset appreciation, tax benefits, and others. But, being honest, if you’re thinking you might move in the next couple of years, renting might be a better option. Or, if the mortgage and utility payments won’t leave you with much cushion for housing or other emergencies, then renting might be the way to go.